While some fraudsters exhibit a true evil genius in covering their tracks, most thieves aren’t that clever. Careful attention to details and review of reconciliations by someone who doesn’t work with that account can help catch many instances of fraud. Stripe offers a powerful reconciliation solution that streamlines the process for businesses. Stripe’s reconciliation solution automates the reconciliation process for businesses and offers a comprehensive picture of your money movement. The card carries no annual fee and has a variable APR, typically ranging from 18.49% to 28.49%. This card is suitable for businesses with limited or poor credit that still want to earn rewards on their spending.

Reasons To Reconcile Bank Statements

The process is particularly valuable for companies that offer credit options to their customers. They can then look for errors in the accounting records for customers and correct these when necessary. In accounting, reconciliation refers to a process a business uses to ensure that 2 sets of accounting records are correct. Although a single-entity small business doesn’t need to consolidate takt time vs cycle time vs lead time the financial statements of multiple entities, companies engaging in M&A will need to complete a consolidation. Accountants’ consolidation processes may use automated ERP software functionality to combine results and remove intercompany transactions or use spreadsheets. Accountants compare the general ledger balance for accounts payable with underlying subsidiary journals.

Streamlining the reconciliation process

The correction will appear in the future bank statement, but an adjustment is required in the current period’s bank reconciliation to reconcile the discrepancy. Analytics review uses previous account activity levels or historical activity to estimate the amount that should be recorded in the account. It looks at the cash account or bank statement to identify any irregularity, balance sheet errors, or fraudulent activity.

Where Do Non-Sufficient Funds (NSF) Checks Go on a Bank Reconciliation?

- Reconciliation is also used to ensure there are no discrepancies in a business’s accounting records.

- Adding to the challenge, sometimes an entry in the general ledger may correspond to two or more entries in a bank statement, or vice versa.

- It helps identify discrepancies caused by outstanding checks, unrecorded deposits, bank fees, or other timing differences.

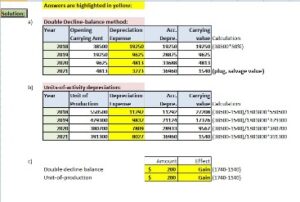

Prepaid assets, such as prepaid insurance, are gradually recognized as expenses over time, aligning with the general ledger. Analyzing capital accounts by transaction, this reconciliation includes beginning balances, additions, subtractions, and adjustments to match general ledger ending balances for capital accounts. It covers aspects like common stock par value, paid-in capital, and treasury share transactions. This reconciliation involves rolling forward fixed asset balances, accounting for purchases, sales, retirements, and accumulated depreciation. It makes sure that fixed asset and accumulated depreciation balances accurately offset each other in the general ledger.

Reconciliation of accounts determines whether transactions are in the correct place or should be shifted into a different account. For example, a company maintains a record of all the receipts for purchases made to make sure that the money incurred is going to the right avenues. When conducting a reconciliation at the end of the month, the accountant noticed that the company was charged ten times for a transaction that was not in the cash book. The accountant contacted the bank to get information on the mysterious transaction.

This highlights the significance of accurate accounting reconciliation in detecting and preventing fraudulent activities within an organisation. By reconciling financial records, such as bank statements, invoices and receipts, businesses can identify discrepancies and irregularities https://www.online-accounting.net/ and protect themselves against potential fraud. Check that all outgoing funds have been reflected in both your internal records and your bank account. Whether it’s checks, ATM transactions, or other charges, subtract these items from the bank statement balance.

Instead of spending days each month reconciling accounts, FloQast AutoRec can do that in minutes. AutoRec leverages AI to reconcile transactions, whether those are one-to-one, one-to-many, or many-to-many. Unlike other reconciliation systems, AutoRec doesn’t require users to create or maintain rules.

Once data is gathered from these sources, the software, through advanced encoding, then compares account balances between documents from the different sources and identifies discrepancies. These are then investigated by accounting staff to identify the main cause of the discrepancies. The perpetuation of fraud https://www.kelleysbookkeeping.com/how-letters-of-credit-work/ is one of the very common problems facing a lot of financial institutions. Even though accounting processes help to monitor every transaction, fraudsters work with accountants to make changes to accounting records. Errors in recording transactions are almost inevitable in the whole accounting process.

This was especially so when the physical legal tender was the main medium of exchange and recipients of money needed to get to deposit points to complete the whole deposit process. Financial statements show the health of a company or entity for a specific period or point in time. The statements give companies clear pictures of their cash flows, which can help with organizational planning and making critical business decisions. The documentation review process compares the amount of each transaction with the amount shown as incoming or outgoing in the corresponding account. For example, suppose a responsible individual retains all of their credit card receipts but notices several new charges on the credit card bill that they do not recognize.

Some of its features include receipt matching, subscription management, and AI-powered spending insights. Ramp is an excellent choice for startups that are aiming to earn rewards on business purchases while managing expenses. The information provided in this article does not constitute accounting, legal or financial advice and is for general informational purposes only. Please contact an accountant, attorney, or financial advisor to obtain advice with respect to your business. An investigation may determine that the company wrote a check for $20,000, which still needs to clear the bank.

The spreadsheet should include beginning balance, additions, subtractions, and any adjustments required for recording to agree with the general ledger ending balances for capital accounts. Make any required adjusting journal entries for general ledger balances to correctly reflect short-term and long-term notes payable components. Compare income tax liabilities to the general ledger account and adjust for any identifiable differences that need recording via journal entry.

In fact, many accountants can enjoy a successful career without having to perform a single account reconciliation. The accounts receivable is an asset that expects a customer to receive an amount. Since the client paid the amount, the accounts receivable (asset) is reduced, therefore crediting the account. Since buying a Mac Studio is an investment (Asset) to the business, the asset increases, debiting a dedicated equipment account. When purchasing the Mac Studio with cash (Asset), the asset decreases as cash goes out of the business; therefore, credit the account. As mentioned earlier, reconciling is a fact-checking procedure commonly employed by a company’s accounts department.

If you’re working for yourself, you (or your accountant or bookkeeper) will perform bank reconciliation. But if multiple people handle your business’s finances, the person reconciling the accounts should probably be different from the person signing the checks. Once these previous steps are completed, you then check that your bank account statement balance is equal to the balance in your internal records.